Using Technology to Help Millennials Own a Home

81 million millennials are said to be homeless

The Ministry of Public Works and Public Housing (PUPR) estimates that there are 81 million people of the millennial generation – who were born between 1980 and 2000 – do not yet own a home. This amount is equivalent to 31% of the population in Indonesia.

In the middle of last year there was a discourse on providing a special mortgage scheme into three groups based on age. First, for those aged 25-29 years, waivers are given for flats or rental apartments.

Second, the age of 30-35 years in the form of subsidies. Finally, those who are over 35 years old, if they already have a permanent job and an apartment according to their salary, this will be discussed how they can be more feasible and comfortable. The government sent representatives to learn about the concept of millennial housing in South Korea.

So far, it's all just talk. On the other hand, the increase in property prices was not matched by an increase in the Regional Minimum Wage (UMR).

Stimulating purchasing power can actually be done by the central bank by loosening the credit limit or by loosening the credit limit Loan-to-Value (LTV) for Home Ownership Loans (KPR). Nevertheless, banks do not necessarily apply it to consumers. There have been adjustments, even months, since the easing was given.

Can it be guaranteed that in that period the purchasing power of consumers will still exist?

Complicated and conventional process

The more you delay the decision to buy, the harder it will be to catch up. Even though the decision to buy a house, for most people, is not an easy matter. From the human side itself, besides price, there are many considerations in terms of location, how close it is to public transportation, main roads, facilities around the house, and much more.

Many have realized that buying a house in Jakarta is impossible. Therefore, the choice fell to the surrounding suburbs.

No one knows that the process of buying a house, especially through a mortgage, is complicated, time-consuming and costly. Because there are no other options offered other than legowo and willing to follow the whole procedure.

Ada booking fees which must be paid for proof of the buyer's seriousness to buy a house so that the agent does not sell the chosen house to another party while waiting for the mortgage process to complete. The amount varies depending on the developer, starting from Rp. 500 thousand for cheap housing, to Rp. 25 million for luxury housing. If a purchase occurs, booking fees can reduce the purchase price.

Next is pay appraisal to the bank or a third party appointed by the bank to assess and estimate the price of the house you want to buy. Same as booking fees, the value varies. Unfortunately, the appraisal money will be forfeited when the mortgage is rejected by the bank.

Appraisal is an important phase because there is an estimation of the price of the house. There are a number of considerations that cause a KPR application to be rejected, for example a location that is not ideal on a skewer, near a cemetery, a garbage disposal, or a pole. This component can make the value of the house low.

Unfortunately, if at this stage the mortgage application is rejected, the money will be forfeited because each bank has its own assessment. That means, have to pay appraisal again if you try a different bank from the first try. This phase takes time, hence the deadline booking fees must also be taken into account.

All financial data of prospective buyers will be seen from the history of BI Checking, if there is a record of bad credit, the bank will be reluctant to provide loans. After this phase is passed, a creditor feasibility analysis will be entered. The bank will survey the prospective creditor's workplace, check the current account, and employment status when taking a non-subsidized mortgage.

Even if you are a permanent employee, the business is not finished. If the working period is under a year, the process is likely to be hampered. If it is passed, there are additional prerequisites. For example, include a work letter from the previous office.

Mediana, a private employee, admitted that her determination to buy a house had existed for many years. He realized that it was time to shift his salary to buy assets, especially the condition of his parents who were getting older. His determination became more determined when encouragement came from his work environment.

"So, yes, it's kind of willing or not willing to go abroad, it's time not to spend money on traveling. But honestly this is because of being influenced by friends. 100% of my mentality at that time was not ready. It's pretty stressful," he told DailySocial.

After much discussion, his determination came true. He decided to buy a house with a location not far from the office and at least affordable by the KRL route. Medio 2017, Mediana began to collect a down payment (DP) of 30% of the house price of Rp437 million. He disbursed all personal savings and was assisted by his parents to pay the down payment.

The credit agreement began in May 2018. At that time, the mortgage installments began. Incidentally, he used BTN for his mortgage because the home developer he chose was a partner of the state-owned bank.

"Incidentally, Indonesia's economic growth was moderate that year slow down, so the interest is lower for lighter installments.”

Starting from the process of looking for a house, the mortgage facility he wants to take, is completely done manually. Alias does not use technology because according to him it has not really provided the right solution. Mediana visited the house at random, including several places she visited.

Suffering has a home

Mediana's story is quite relevant to the released global research HSBC with Kantar TNS. This research states that around 36% of millennials who already own a house in various parts of the world receive financial assistance from their respective parents.

In Canada, the share is similar to the global figure, which is 37%. In the United Arab Emirates, the figure is much higher, at 50%. France is at the lowest, only 26% of millennials buy a house with the help of their parents.

This research involved 9.009 respondents from nine countries, namely Australia, Canada, China, France, Malaysia, Mexico, United Arab Emirates, United Kingdom and United States.

As many as 70% of millennials in China already own a home, placing this country the highest of the eight other countries. In the US, the figure is only 35%. While in Australia, the figure is much smaller, at 28%.

More than half of the respondents stated that they were willing to cut their lifestyle costs and have fun in order to own a house. They are willing to cut down on hanging out in cafes or shopping for clothes. Not only are they thrifty, they are also willing to go through various hardships in order to be able to buy a house.

As many as 21% of millennials said they were forced to postpone having children. As many as 33% choose a house that is much smaller than desired. Then, 18% of millennials are willing to buy a house that they don't really like, for example, it's too far from their place of work. In fact, there are 21% of millennials who say they rent out some rooms to help pay their installments.

Watching the development of proptech

Technology is designed to make decisions easier. The same is also applied when buying property, which in fact should not be absent with the presence of technology. How is the development of technology for property so far?.

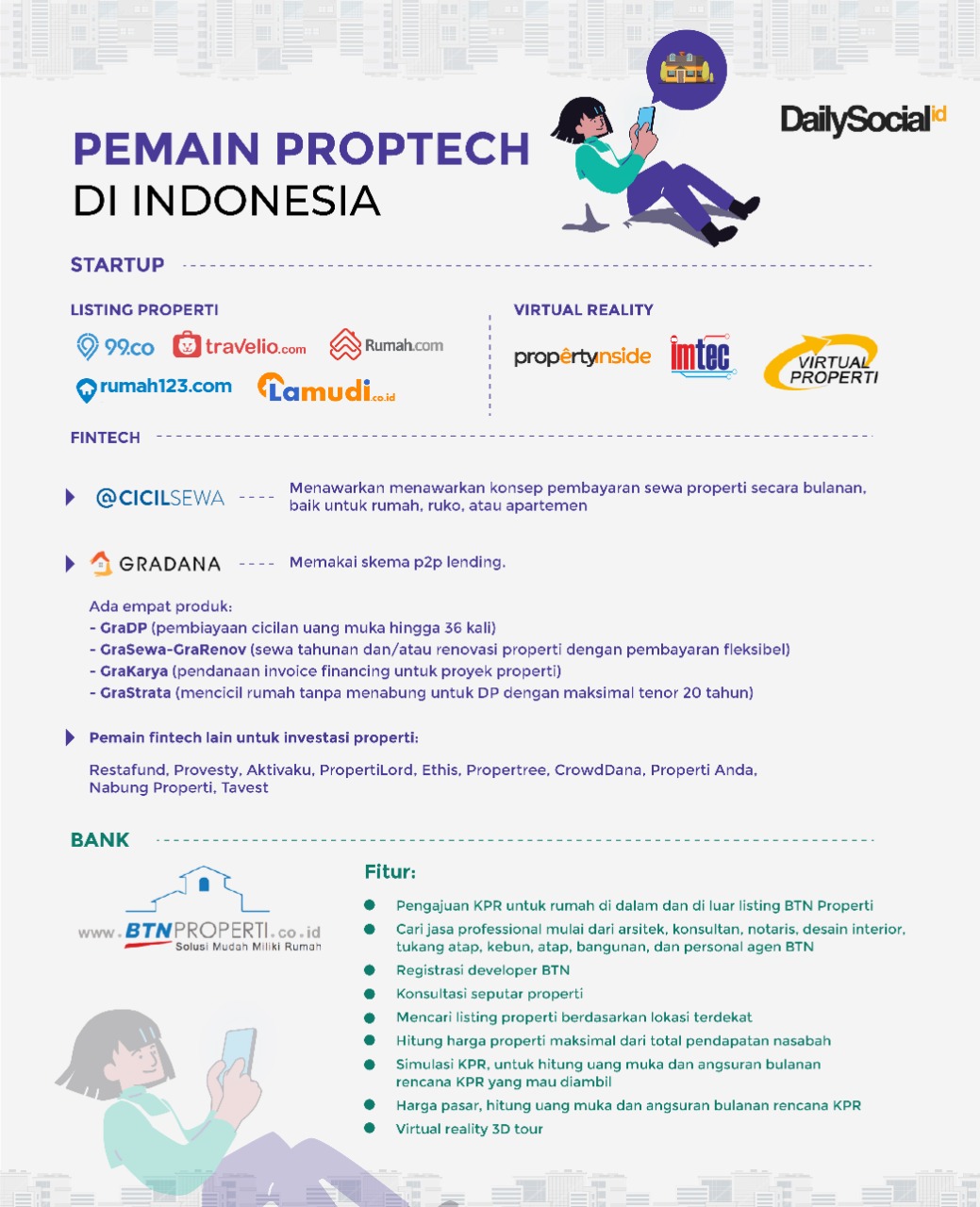

From the startup realm, now there are several players who focus on property or for short proptech. Definition proptech is the use of information technology to assist in the search, purchase, sale, and management of real estate.

When translated into business language it becomes, listing property, platform Virtual Reality, leasing, to property financing. Almost all vertical proptech already present in Indonesia, but mostly playing in listing, leasing, and financing.

In the realm listing, there are Lamudi, Travelio, Rumah123, 99.co, and Rumah.com. Although each of these players began to enter other verticals, for example Travelio which helps property owners to manage it. Rumah.com provides a mortgage calculator to help with simulations and additional information to enrich the user's treasures.

Meanwhile, in the realm of funding, there are CicilSewa and Gradana, both of which focus on property financing. CicilSewa offers the concept of paying property rent on a monthly basis, whether for houses, shop houses, or apartments. The problem they want to solve is being required to pay rent in advance for a year or two.

Meanwhile, Gradana utilizes a p2p lending scheme for non-bank mortgage loans, including loans to pay a down payment when applying for a mortgage. This solution can be said to be revolutionary, considering the risks are quite high.

Through one of its products, namely GraStrata, a choice of tenors of up to 20 years is provided. As one of the risk management measures, the company requires borrowers to deposit 2% of the loan value and it will be returned after paying it off.

The solution provided by this proptech startup is quite a relief because they are able to answer the pain points that continue to haunt potential home buyers. What about the banking itself?.

You can take an example from the state-owned bank BTN. They are banks specifically designated by the state to focus on housing finance. So naturally, all of its products are specifically designed to make it easier for customers to take mortgage installments.

Their commitment to improving business through technology is commendable and ambitious. BTN developed the concept proptech through the site and application BTNProperty. There are property search menu options, submissions, consultations, to looking for professional services ranging from architects, consultants, notaries, interior design, roofers, gardens, roofs, buildings, and personal BTN agents.

The application also provides a mortgage calculator to calculate the down payment and monthly installments for the mortgage plan, or calculate the maximum property price that can be purchased from the customer's total income. Even there, you can apply for a BTN KPR, it is claimed that the process only takes 10 minutes.

KPR products from BTN here are quite diverse, there are new KPR/KPA, Home Collateral Credit, KPR Second, mortgage Take Over, Light Loans, and KPR Gaeess specifically for millennial customers. KPR Gaeesss has been released since October 2018 targeting millennials aged 21-35 years. Down payment starts from 1%, free of admin fees, fixed interest rate of 8,25% for two years, 50% discount on provision, and a tenor of up to 30 years.

The concept of BTN The property offered by BTN is quite interesting. The data bank that is so abundant is actually very useful for increasing utilization in order to be able to mix the products needed by customers. The more relevant the solutions offered are the solutions offered.

"We think this is a serious problem. There is a gap between the current housing sector and developments in society, where the current productive age is increasingly dominated by the millennial generation whose habits and service needs are slightly different. We as the main players [in housing finance] must understand this condition very well," said BTN President Director Pahala N Mansury as quoted from NewsEconomy.

Hope on the government

Banking products such as those offered by BTN can indeed break the impasse in access to finance for the present generation. But the real hot ball is in the hands of policy makers. Strict regulations are the key to showing the government's alignment so that today's young generation can have their own affordable housing in terms of price and distance.

Property observer Alviery Akbar explained that currently the central and local governments still have the largest land area in the city. That is why further intervention in this matter can only be done through regulation. The Associate Director of Residential Sales & Leasing at Colliers International Indonesia said strict regulation was the key so that affordable housing for the younger generation would not be damaged by speculators.

“So if you want to intervene through government regulations that are specifically for making housing for the younger generation with very strict requirements to avoid investors/speculators. The role of banks that provide KPA/KPR can intervene by selecting buyers according to the stipulated requirements,” said Alviery.

The DKI Jakarta Regional Government has provided an example of how regulatory intervention is needed to solve problems in the property sector. This was reflected at the end of 2018 when Governor Anies Baswedan signed a Governor Regulation Number 132 of 2018 regarding the Management of Owned Flats. Through this gubernatorial regulation, the government patched legal loopholes that are often played by developers through fee collection or other management.

Plans on paper are always easier than their implementation and policy formulation will always intersect with political interests. If the local and central governments decide to make affordable housing for the younger generation, Alviery said the government must find another way out for a number of residents who are at risk of losing their homes due to government projects, such as people living on riverbanks or those affected by infrastructure development.

Relying on the role of the private sector is like longing for the moon. The very high land prices and the very commercial nature of property developers are the most basic reasons that there will be no property worth IDR 500 million built by private developers.

"Every inch of land owned is very valuable, even if you have to build a dwelling, it is more profitable for the upper middle market which will bring maximum profit," concluded Alviery.

Despite the government's role, technology in this property industry continues to develop. Although it has not solved the main problem, the present generation can at least take advantage of the available technology to obtain credit or simply access essential information before buying a house, as has been offered by a number of proptech and BTN.

Sign up for our

newsletter

Review Order

Monthly

IDR 150.000

Payment Details

Subscribe Monthly

Total payment

By clicking the payment method button, you are read and

agree to the

terms and conditions of Dailysocial.id