Fintech Company Competition and Conventional Loans in the Middle of the Southeast Asian Market

Competition intensifies as digital services outpace legacy financial systems.

Southeast Asian tech giants are in an intense battle with major conventional banks over the region's growing digital banking services.

The “superapps” like GoTo and Grab want to increase the reach of their banking services, and existing players use this region as sandbox for digital experimentation, populations in long-neglected areas may soon have access to some of the world's most technologically advanced financial services firms.

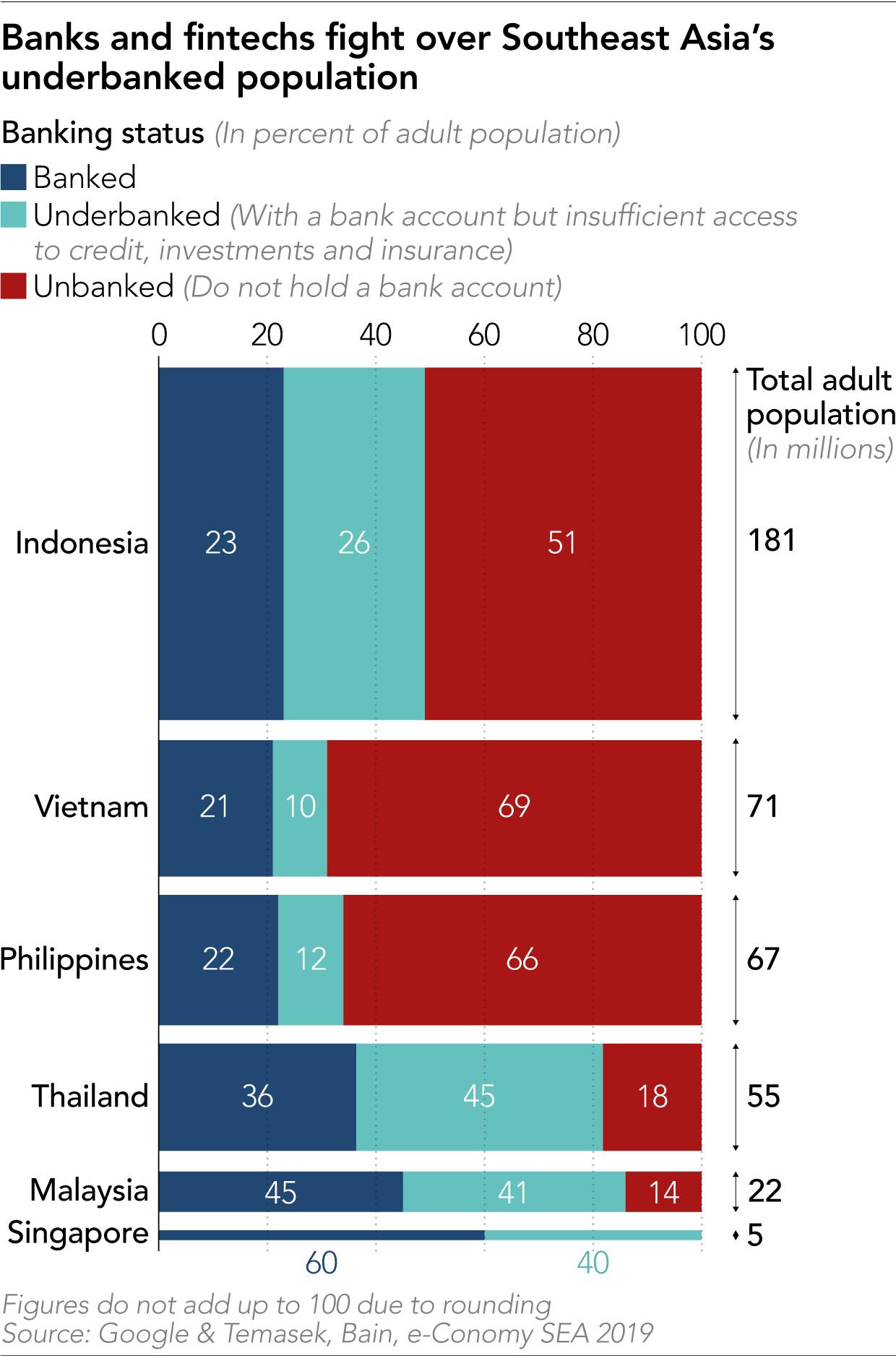

According to research conducted by Google, Temasek Holdings and Bain & Co., about half of Southeast Asia's nearly 400 million adults are unbanked. Over 90 million more are “underbanked”: They have bank accounts but do not have adequate access to investment, insurance or credit products. Millions of small and medium-sized businesses also face significant funding gaps, according to the study.

The problem is particularly thorny in Indonesia, where more than 70% of adults—about 140 million people—do not have bank accounts or unbanked, partly because of the cost of offering traditional services. Building a physical banking network, such as branch offices and ATMs, to cover an archipelago of 17.000 islands to serve a largely low-income community has proven nearly impossible.

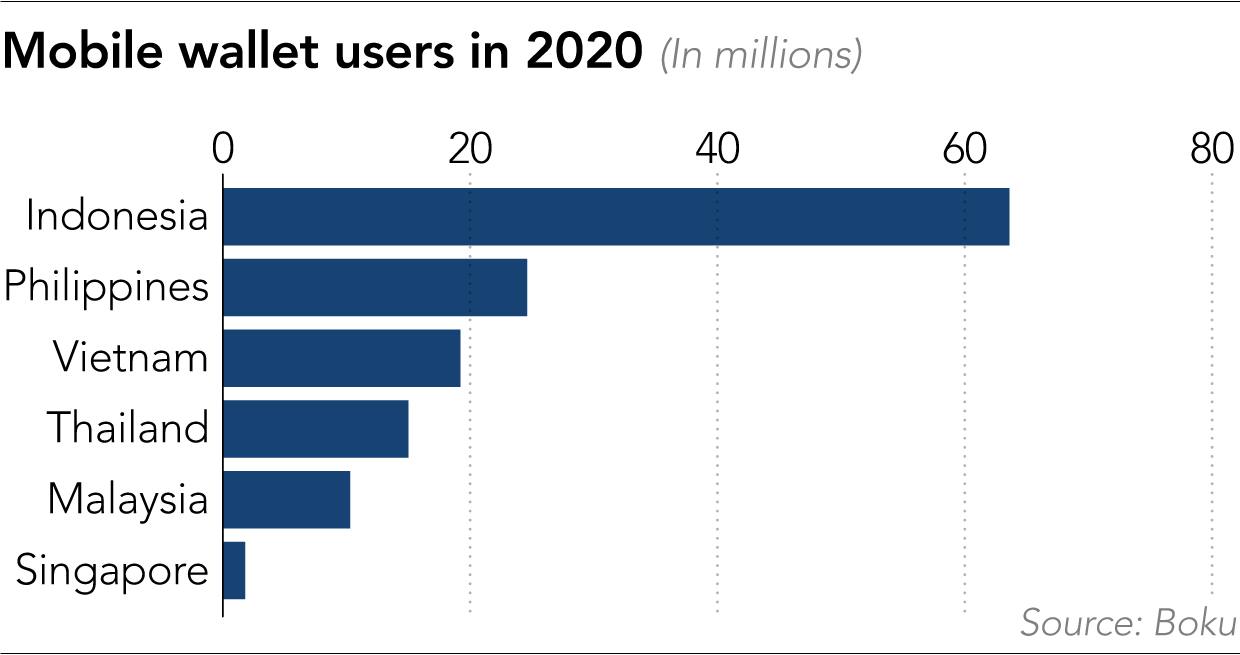

But the country's rapid adoption of smartphones is changing the industrial landscape. GoTo, Indonesia's largest technology conglomerate, will soon offer fully integrated banking services with its local partner, Bank Jago, in direct competition with digital innovations from conventional banks, including Singapore's DBS Group Holdings and United Overseas Bank (UOB).

Graphics by Nikkei Asia

Graphics by Nikkei AsiaFor GoTo, which was formed through the merger of two of Indonesia's most prominent technology companies, providers of online transportation services Gojek and e-commerce giant Tokopedia, the expansion is a natural extension of the services already offered through its superapp.

Its e-wallet service, GoPay, allows customers to make cash deposits at convenience stores and use the app to make purchases, access credit through a “buy now, pay later” scheme, and even make microinvestments in US index funds and gold.

Gojek bought a 22% stake in Bank Jago, a local bank, at the end of last year. Together they plan to offer a wide range of banking services. GoPay customers in Indonesia will soon receive a message saying, “Open a Bank Jago account”, which they can easily set up right from the app. The cash already in their e-wallet can be used as their first deposit. Customers will soon receive a Visa debit card and access to investment options. This includes discount benefits for products sold on Tokopedia.

The service looks like a combination of Amazon.com, Robinhood, PayPal, and Citibank, all in one app. The company's main goal "is to be at the core of how users manage their finances," said Budi Gandasoebrata, GoPay's managing director.

GoTo also plans to offer similar banking services to small and medium businesses that use the service Gojek and Tokopedia. "That's where we see [the service], hopefully, in the next five years," Budi added.

It is not difficult to see why Indonesia has become the focus of innovation and competition in the banking sector. The country is the most populous in the region and half of the population is 30 years or younger, one of the most digitally savvy. According to the Boston Consulting Group, this will drive the second-highest rate of e-payments in Southeast Asia, after Singapore, by the end of 2019. The number of middle-class and upper-class consumers in Indonesia is expected to grow by 130% between 2019 and 2024. During the same period, revenue banking sector is expected to increase from USD 47 billion to USD 77 billion.

Earlier this year, Singapore-based internet giant Sea, which provides e-commerce and e-wallet services that compete directly with GoTo, took majority control from a small Indonesian lender called Bank Kesejahteraan Ekonomi, which was later renamed SeaBank. Akulaku, an Indonesian fintech startup backed by the Ant China Group, also joined the crisis, becoming the largest shareholder in Bank Yudha Bhakti, which later changed its name to Bank Neo Commerce.

However, the banks incumbent Large companies in Southeast Asia, such as DBS and UOB Singapore, have already provided digital banking services in the region.

UOB launched the digital bank TMRW in Thailand in 2019, and in Indonesia the following year. This service has acquired more than 400.000 users.

Graphics by Nikkei Asia

Graphics by Nikkei AsiaJanet Young, Head of Group Channels and Digitization UOB, said the company is well aware of the increasingly fierce competition from tech giants. “We see them as competitors because they have an ecosystem … but have fewer regulatory requirements because they are not banks. Running a bank with all its intricacies, all the regulatory guidelines—managing a balance sheet is different from just being an e-wallet,” he said.

In contrast to newcomers, Janet said TMRW is designed to serve the region's young professionals, such as those “who have graduated from college and found a job, or someone who has worked for a number of years, and digitally savvy customers especially those who prefer mobile. ”

Janet stressed that UOB was not using its digital banking services as a “defensive measure” to fend off the tech giant. Instead, he says, “we are using TMRW as a [customer] acquisition strategy. This is a lower cost acquisition for us, compared to the core [business]. Digital banks are much more scalable and cost-effective.”

UOB also uses TMRW as an innovation laboratory, which it believes will strengthen core banking services in developed markets such as Singapore. Last month the company announced plans to invest SGD 500 million (USD 371 million) in digital services and to integrate its digital banking capabilities from TMRW and its main banking app used in countries such as Singapore. The bank said that it is “trying to double the retail customers it serves digitally to more than 7 million customers across ASEAN by 2026.”

“Consumer behavior tends to be digital. If we are not digital, we will lose the ability to serve them,” added Janet.

The crisis between banks and fintech companies will also heat up in UOB's domestic market. Superapp provider based in Sea and Singapore, Grab, plans to launch digital banking services in the city early next year. Analysts say the players bring great but different strengths to the fight.

"Financial institutions incumbent in digital banking services have the advantage of obtaining financing for investment, as they have more collateral and a better reputation, and existing relationships with creditors and investors,” said Gavin Yue, research consultant at Kapronasia, a fintech-focused consultancy. company.

“They also have better access to internal funds, which implies that they are better capitalized. This can impact, for example, marketing, pricing and acquisition initiatives.”

But “on the other hand, digital startups have a more flexible data infrastructure, unlike legacy institutions which have to grapple with layers of old technology, which undermines data analytics and subsequently the products, services, and overall experiences that [they] can provide to consumers,” Gavin added.

“The entry of technology startups is like Grab or Sea is an ambitious thing, but at the same time calculated. Driven in large part by the pandemic, consumers are increasingly looking to digital channels to complement almost all aspects of their lifestyle.”

The fintech revolution in Southeast Asia is forcing other players in the financial ecosystem, such as Visa and Mastercard, to adapt.

“In any given year, we partner with 50 to 60 fintech companies in Asia-Pacific,” said Matthew Wood, who oversees Visa's digital and fintech partnerships in the region. Tobias Puehse, vice president for innovation and customer solutions for Mastercard's Asia-Pacific business, said that "evolving markets" — those whose customers are abandoning legacy banking structures and embracing mobile apps and digital payments first — "will always give us a glimpse of what the consumer behavior ."

The two payments companies are competing fiercely in the region to expand their partnerships beyond traditional banks. Visa invests in Gojek in 2019 and Mastercard are partners Grab. According to Visa, less than half of consumers in Southeast Asia see cash as their preferred payment method. “Ultimately, our goal is to eliminate cash, and fintech can and will be a huge driver for moving commerce in Southeast Asia to become increasingly digital,” said Matthew.

The series of computer crashes faced this year by Japanese bank Mizuho, including one that brought most of its ATMs to a temporary halt, is a reminder of the difficulty of upgrading derivative systems, while closing core branches in established markets such as the US incurring long-term restructuring costs. short, even if it saves you money in the long run.

But players in Southeast Asia's new and incumbent financial sectors are demonstrating that they can build app-specific digital banking infrastructure, almost from scratch, in countries like Indonesia — an example of a leap. As Yue from Kapronasia said: “Of course competition from new players will benefit consumers.”

-This article was first released by Nikkei Asia, republished by Krasia. Re-released in Indonesian as part of the collaboration with DailySocial

Sign up for our

newsletter

Review Order

Monthly

IDR 150.000

Payment Details

Subscribe Monthly

Total payment

By clicking the payment method button, you are read and

agree to the

terms and conditions of Dailysocial.id